CURRENT STATE

The role of technology in support of learning has morphed from what used to be a handful of authoring tools and a learning management system, to complex, multi-layered technology stacks often referred to as learning ecosystems. While authoring tools and Learning Management Systems are still important components, they are no longer alone.

Authoring tools (45%) and learning management systems (42%) still lead the pack. Even many smaller companies now feature an LMS though the market appears far from saturated for mid-size businesses.

- Social learning platforms have become mainstream ecosystem components with 33% of respondents claiming to own one. 28% of respondents feature have a video platform and 26% have a learning content management system. Not far behind are microlearning platforms at 24%. More than 20% own learning operations platforms and coaching/mentoring platforms. This indicates a solid growth trend and wide acceptance in all these technologies.

- The fact that learning analytics tools are near the bottom in popularity at 14% may be one indicator of why Learning and Development (L&D) continues to struggle with learning measurement as a significant challenge.

- At 6%, augmented and virtual reality tools lag behind. Despite their promise, AR/VR are still fringe technologies and more commonly found in large companies or enterprises.

COMPLEXITIES

When we asked respondents about top challenges to their learning organizations, only 20% selected “Constraints with our technology.” However, when we looked closer at the data, we found enterprise-sized businesses (15,000 employees or more) found this to be a far more resonant challenge.

CONSEQUENCES

Across all sizes of business, with the exception of large enterprises, respondents expect either an L&D budget increase (61.4%) or for the budget to stay the same (26.1%), a far more hopeful outlook than in our last benchmarking survey conducted in 2020.

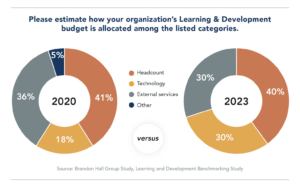

Comparing benchmarking data from 2023 versus 2020, the technology allocation in L&D budgets has increased 12.5%, to a robust 30%. That’s good news for learning technology providers.

Where do learning organizations plan to spend their technology budget allocations? Social learning or collaboration platforms topped the list with almost one-third indicating an intention to buy over the next year. Content creation is a critical driver for approximately 1/4 of respondents, who are looking for authoring tools (27%), LCMSs (26.1%) and video platforms (23.3%). Also in demand are coaching/mentoring platforms (22%) and learning operations platforms (20%).

AR/VR tools (11%) and learning analytics (10%) are the least desired technology purchases. AR/VR has yet to become a mainstream modality, and learning analytics platforms, despite learning measurement being the top challenge reported by our respondents, simply do not seem to warrant much budgetary interest.

CRITICAL QUESTIONS

- Do you have a strategy to explore, assess, and select learning technologies that address not just costs but learning effectiveness, business case, and integration with your existing learning ecosystem?

- How effective is your current learning technology stack? Are there any critical gaps?

- Does your learning budget allocation percentage measure up against the reported average of 30%? If you ask for more can you make a clear business case for the budget increase?

- Social learning functionality is clearly a hot technology at the moment and is rated as instructionally effective. Is it missing from your learning technology stack?

BRANDON HALL GROUP POV

For today’s learning and development organization, navigating the learning technology space can be a daunting task. New learning technologies are constantly finding their way into the market, and technology vendors are rapidly merging, making acquisitions, and adapting and expanding their offerings to keep pace with their competitive peers. It’s a steep challenge for an L&D organization to keep up, and an even steeper one to sift through this ever-evolving market and identify which learning technologies it makes sense to add given your organization’s needs, budget, and existing technology stack.

It’s incumbent upon L&D organizations to invest the time and resources to learn about the learning technology space and keep abreast of its ever-evolving offerings and their capabilities. While learning budget outlooks are rosier than in years past, it’s always easier to persuade executives and budgetary decision-makers with a business case that addresses organizational impacts, not just instructional effectiveness. Certainly, technology vendors can provide some information to guide the creation of a business case based on their other clients, but it is up to the L&D team to paint the picture of what a new set of learning functionality can realistically achieve for their organization.